The Quarter Klarna Started Making Money

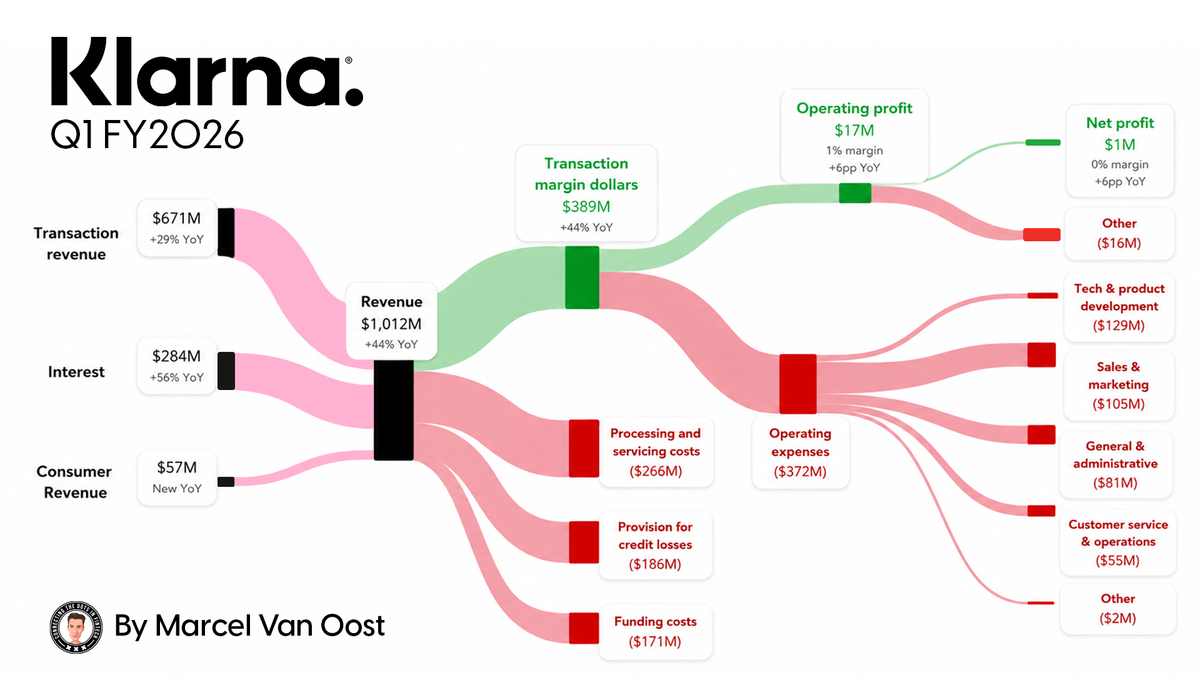

Klarna's first quarter of 2026 will be remembered as the one where profitability quietly stopped being a question. The Swedish FinTech crossed $1 billion in quarterly revenue for the first time, swung to a positive net income of $1m against a $99m loss a year ago, and posted adjusted operating profit of $68m, up from a rounding-error of $3m in Q1'25.

All of this while GMV growth accelerated, which is the part that should make competitors uncomfortable. The narrative Klarna has been selling to investors since its IPO, that it is a spend-centric network, not a lender, is now showing up in the P&L.

Key Q1 2026 Figures

Growth accelerated and profitability arrived in the same quarter, which is a rare combination worth breaking down:

- GMV reached $33.7 billion (+33% YoY).

- Revenue hit $1.0 billion (+44% YoY)

- Transaction margin dollars also grew 44% to $389 million.

- Adjusted operating profit surged to $68 million, up from just $3 million in Q1 2025.

- Operating income turned positive at $17 million, reversing a $99 million operating loss a year prior.

- Active users grew 21% YoY to 119 million.

- Key signal: adjusted operating expenses grew only 20% while revenue grew 44%.

The Growth Engine: Fair Financing

The standout growth driver is Fair Financing, Klarna's POS installment product.

Its GMV grew 138% year-over-year to $4.1bn and now represents 12% of total volume.

Because interest income accrues over the life of these loans, the effect compounds: interest income reached $284m, up 56% YoY, and Klarna booked an additional $57m gain on sale from offloading $1.2bn of Fair Financing receivables.

Crucially, most POS installment borrowers arrive with an existing Pay Later repayment history, so Klarna is deepening monetization of consumers it already underwrites rather than chasing riskier new ones.

Geographically, the US is Doing the Heavy Lifting

US revenue grew 67% (versus 32% outside the US) and US GMV rose 39% to $7.1bn. Two other lines deserve attention from anyone modeling the business.

Consumer membership revenue grew nearly six-fold year-over-year, and the Klarna Card now has 5m active users across 16 countries, pushing Klarna into everyday spend well beyond the checkout button.

Cost Discipline: Operating Leverage, Not Cuts

This is where the story is more interesting than a simple "costs fell" headline. The point is the gap. IFRS non-transaction-related operating expenses grew just 3% year-over-year while revenue grew 44%. This operating leverage is attributed to AI-enabled productivity gains and continued restraint on headcount-driven spend. Sales and marketing rose only 9%, and customer service and operations only 7%, both growing far slower than the network they support.

Transaction costs did climb 45%, but that shouldn't set off alarm bells: it reflects the mix shift toward Fair Financing, which carries higher servicing costs, and upfront card-issuing costs, both tied directly to revenue-generating activity.

Funding costs grew a comparatively modest 32%, cushioned by the deposit-led model: $12.3bn of consumer deposits fund 90% of the balance sheet, the majority long-term fixed European deposits that hand Klarna a durable structural cost advantage.

What's Next Operationally

The distribution flywheel is the story to watch. Klarna is now live and ramping as a default option with Stripe and Nexi, with JPMorgan Payments and Worldpay scheduled to follow during 2026, PSP partners that collectively process over $9 trillion in annual volume.

The deeper Stripe integration, plus a new tie-up with Google Gemini, plants Klarna firmly inside the emerging agentic-commerce stack. On the balance sheet, expanded forward-flow agreements let Klarna keep selling receivables, transferring credit risk and accelerating revenue recognition while staying capital-light.

Management reiterated FY26 guidance of >$155bn GMV and guided Q2 revenue of $960m–$1,000m with adjusted operating profit of $30m–$50m, flagging that provisions will rise through the year purely on seasonality.

Where Klarna Is Headed

The core idea is simple: Klarna lends small amounts for short periods, the average balance is just $124, and the whole loan book cycles through roughly ten times a year.

Then it re-checks a customer's creditworthiness on almost every purchase. That makes it structurally safer and easier to scale than a traditional credit card, which lets people carry large balances for months.

Q1'2026 is the first quarter where that model delivered real profit and faster growth at the same time. If Klarna keeps growing its transaction margin faster than its costs, which is exactly what management expects, the right comparison stops being other buy-now-pay-later players and starts being the big payment network it increasingly resembles.

Sources

Comments ()